Summary of Finance Bill 2018-19 Clauses

08 November 2018

08 November 2018

On Wednesday 7th November 2018, Government published the final version of the Finance Bill 2018-19 legislation and explanatory notes that will now make its passage through Parliament to obtain Royal Assent in order to take effect in the 2019-20 tax year and subsequent years. Some of the key provisions are:

Part 1 Clause 10 – Exemption for expenses related to travel

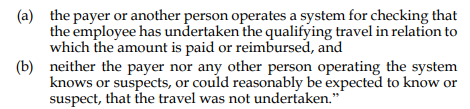

Section 289A of ITEPA 2003 (exemption for paid or reimbursed expenses) has been amended to remove the requirement for employers to check receipts where expenditure has been incurred by employees using the HMRC benchmark scale rates to pay or reimburse their employees’ qualifying subsistence expenditure. Subsection 4A is inserted into Section 289A which introduces “Condition C”;

Therefore, employers must now ensure that there is a system for checking that the employee has undertaken the qualifying travel and there is no reason to know or suspect that the travel was not undertaken. This is an easement from the current checking regime which requires proof of the expense having been incurred, and means that receipts will no longer need to be seen.

Qualifying travel is defined in new subsection 5A as “travel for which a deduction from the employee’s earnings would be allowed under Chapter 2 or 5 of Part 5”.

This clause also allows HMRC to include a statutory exemption for overseas scale rates, subject to the same checking requirement as benchmark scale rates.

Part 1 Clause 7- Optional remuneration arrangements (‘OpRA’): arrangements for cars and vans

This clause introduced amendments to OpRA legislation introduced in Section 7 and Schedule 2 to the Finance Act 2017. Section 120A of the Income Tax (Earnings and Pensions) Act 2003 (‘ITEPA’) is amended to clarify the amount foregone when a taxable car or van is provided though OpRa. The amount foregone in connection with a car or van for a tax year includes the costs connected with the car or van which are regarded as part of the benefit in kind under normal rules. The changes adjust the value of any capital contribution towards a taxable car when the car is made available for only part of the year.

Part 1 Clause 38 and schedule 15 – Entrepreneur’s relief

Chapter 3 Part 5 of Taxation of Chargeable Gains Act 1992 (transfer of business assets: entrepreneurs’ relief) has been amended via Schedule 15 of the Finance Bill which confirms the entrepreneur relief changes announced by the Chancellor at the Budget 2018:

1. The individual must be entitled to at least 5% of the company’s distributable profits

2. The individual must have a right to at least 5% of the net assets of the company available to equity holders on a winding up

Part 4 Clause 81 – Construction Industry Scheme (‘CIS’) and Corporation Tax Securities

The clause inserts section 70A into Chapter 3 Part 3 of the Finance Act 2004 which grants HMRC powers to make secondary legislation to require a person to provide a security for tax liabilities and CIS deductions that a person is or may be liable to pay to HMRC. HMRC may use this power if a HMRC officer considers it necessary to protect revenue.

Regulations must offer a right of appeal against the decision to require the security and in terms of the amount, terms or duration of any security required.

Failure to pay a security will be a summary offence and the person who has committed the offence will be subject to a fine.

Securities are typically required where a taxpayer has a poor compliance or payment record and in “phoenix” cases whereby a business accrues owes liabilities, goes into liquidation or administration and the person responsible for the operation begins to operate under a new company, with the risk of running up further debts.

HMRC already possess powers to require a security for VAT and PAYE.

Part 1 Clause 16 and schedule 4 – Tax Avoidance involving profit fragmentation

Schedule 4 introduces new anti-avoidance legislation to ensure that business profits cannot be taken out of the charge to UK tax by arranging for them to be attributed abroad to offshore persons or entities with lower tax rates. For corporation tax purposes this has effect from 1 April 2019 and for income tax purposes this has effect from 6 April 2019.

See the full version of the Finance (No.3) Bill here and the accompanying Explanatory notes here.