13.01.16 Have you forgotten about Section 289A ITEPA? Are your Umbrella Contracts Caught by the amended definition of a relevant salary sacrifice?

13 January 2016

13 January 2016

Have you forgotten about Section 289A of the Income Tax (Earnings and Pensions) Act 2003 (‘ITEPA’)? Let me remind you…

Section 289A ITEPA 2003 is a section of the legislation, introduced in the Finance Act 2015 that will be effective from April 2016, to replace the prior expense dispensation. It allows for an exemption for paid or reimbursed Chapter 2 or Chapter 5 of Part 5 of ITEPA expenses but specifically excludes expenses which are paid via a salary sacrifice arrangement.

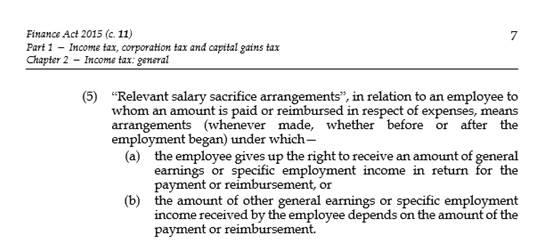

This was all well and good, however at the eleventh hour the legislation was amended so that the definition of a relevant salary sacrifice was amended to include the sub clause (5) (b);

This description is perceived as intended to catch a standard umbrella arrangement where the payment of profit related pay or bonus is dependent upon the amount of expenses paid.

2016 is here and you are probably busy thinking of your strategy Post April 2016 in relation to Finance Bill 2016 draft clauses, predominantly Section 339A of ITEPA 2003, however Section 289A is potentially a bigger challenge!

Are you intending to continue to pay expenses post April 2016? Will your Contracts and payroll calculation be caught by this definition of a salary sacrifice?

If you want to discuss this further, please do not hesitate to contact us at Aspire Business Partnership LLP on 0121 445 6178 or email us at enquire@aspirepartnership.co.uk.